March 23, 2026

Enterprise

Multi-Vendor

PIM

Managing payments across multiple vendors in enterprise marketplaces presents complex challenges that directly impact cash flow, compliance, and customer satisfaction. Enterprise ecommerce leaders must navigate split payment architectures, global regulatory requirements, and automated settlement workflows while maintaining operational efficiency at scale. This comprehensive guide delivers actionable strategies for implementing optimised multi-vendor payment systems that reduce friction, ensure compliance, and accelerate marketplace growth. You’ll discover proven frameworks for selecting payment models, automating compliance, managing disputes, and leveraging AI-powered platforms to drive measurable improvements in transaction success rates and vendor satisfaction.

Table of Contents

Key takeaways

Understanding multi-vendor payment models and their implications

Setting up compliance and automation for secure multi-vendor payments

Managing refunds, disputes and multi-currency challenges efficiently

Leveraging AI and pre-built payment platforms to enhance marketplace efficiency

How Ultra Commerce supports your multi-vendor payment strategy

FAQ

Key Takeaways

Point | Details |

|---|---|

Core payment models | Understand aggregated, split and hybrid models to pick the right architecture for speed, compliance and vendor relationships. |

Compliance and AI | Prioritise PCI, PSD2 and KYC processes and deploy AI driven fraud detection to protect payments. |

Refunds and disputes | Establish clear workflows for refunds, chargebacks and dispute resolution to keep customers satisfied and cash flow predictable. |

Ready made platforms | Leveraging ready made platforms reduces development time and total cost while maintaining governance and compliance. |

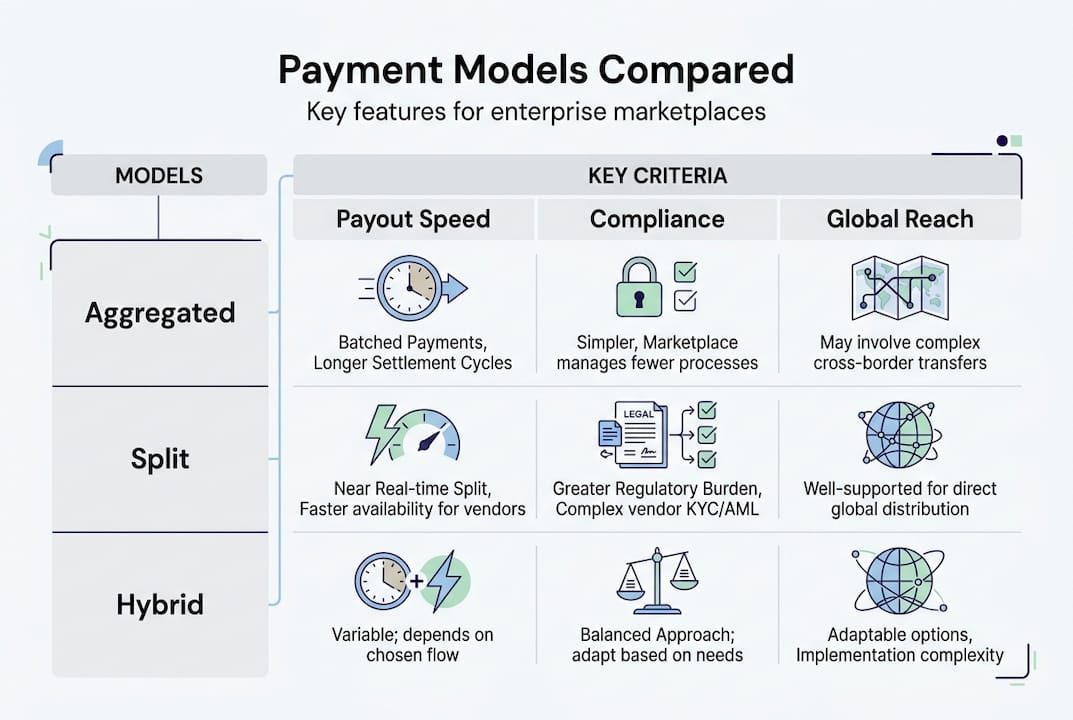

Understanding multi-vendor payment models and their implications

Selecting the right payment architecture shapes your marketplace’s operational efficiency, vendor relationships, and compliance posture. The three primary models each offer distinct advantages that align with different enterprise priorities and growth trajectories.

Aggregated payment models dominate the landscape, with 62% of global marketplaces using this approach where the platform collects all customer payments and distributes funds to vendors on predetermined schedules. This model simplifies initial setup and reduces compliance complexity since the platform acts as a single merchant of record. However, vendors experience delayed access to funds, typically waiting days or weeks for scheduled payouts. The platform assumes greater liability for transactions and must manage working capital to cover the gap between customer payment and vendor settlement.

Split payment systems enable real-time, automatic fund distribution directly to vendor accounts at the point of transaction. This approach improves vendor cash flow and reduces platform liability by routing payments immediately. The trade-off involves significantly higher compliance requirements, as each vendor must complete individual onboarding with KYC verification, tax documentation, and payment processor approval. Split payments face global availability limitations and increased technical complexity in managing multiple payment relationships simultaneously.

Hybrid models combine elements of both approaches to balance operational needs with regulatory requirements. Platforms might use aggregated payments for smaller vendors while offering split payments to high-volume sellers, or vary the model by transaction type or geographic market. This flexibility supports diverse vendor ecosystems but requires sophisticated payment orchestration to manage multiple workflows.

Pro Tip: Evaluate your vendor composition and growth trajectory before committing to a payment model. Marketplaces planning rapid international expansion often benefit from starting with aggregated payments to minimise compliance friction, then migrating high-volume vendors to split payments as relationships mature.

Payment model | Payout speed | Compliance complexity | Global availability | Best for |

|---|---|---|---|---|

Aggregated | Scheduled (days to weeks) | Lower | Universal | New marketplaces, diverse vendor base |

Split | Real-time | Higher | Limited markets | Established vendors, high-value transactions |

Hybrid | Variable | Medium to high | Depends on mix | Large-scale platforms with tiered vendors |

When choosing marketplace software, assess these model characteristics against your operational priorities. Consider vendor expectations around payment timing, your capacity to manage compliance overhead, and whether your target markets support your preferred payment architecture. The digital transformation of shopping centres demonstrates how traditional retail environments successfully adapted payment systems to support multi-vendor operations, while transforming online retail requires similar strategic payment decisions.

Setting up compliance and automation for secure multi-vendor payments

Regulatory compliance forms the foundation of trustworthy multi-vendor payment operations. Enterprise marketplaces must satisfy multiple overlapping requirements that vary by jurisdiction, transaction type, and vendor location.

PCI-DSS certification ensures secure handling of cardholder data across all payment touchpoints. Your platform must implement tokenisation, encryption, and secure data storage regardless of whether you choose aggregated or split payment models. PSD2 regulations govern payment services in European markets, mandating strong customer authentication and open banking compatibility. KYC and AML procedures verify vendor identities and monitor transactions for suspicious patterns, protecting your platform from fraud and regulatory penalties.

The merchant of record decision carries significant implications for liability and compliance responsibility. When your platform acts as MoR, you assume legal responsibility for transactions, simplifying vendor onboarding but increasing your regulatory burden. Intermediary models distribute compliance obligations across vendors, reducing platform liability but creating friction in vendor acquisition. Payment processing platforms report that 57% of providers now invest in AI-powered fraud detection to manage these risks effectively.

Automation platforms like Stripe Connect, Adyen for Platforms, and Ryft eliminate manual commission calculations and payment splits that create operational bottlenecks. These systems handle complex scenarios including tiered commission structures, promotional fee waivers, and dynamic pricing rules while maintaining audit trails for financial reconciliation. Automated split calculations reduce errors that damage vendor relationships and ensure accurate tax reporting.

AI-powered fraud detection analyses transaction patterns in real-time, flagging suspicious behaviour before funds settle. Machine learning models identify anomalies across multiple data points including device fingerprints, purchase velocity, shipping addresses, and historical vendor performance. This proactive approach reduces chargebacks that erode profit margins and damage payment processor relationships.

Critical compliance checkpoints for enterprise marketplaces:

Complete PCI-DSS Level 1 certification for platforms processing over 6 million transactions annually

Implement strong customer authentication meeting PSD2 requirements for European transactions

Establish automated KYC workflows collecting government identification, tax information, and business verification

Deploy real-time AML monitoring scanning transactions against sanctions lists and suspicious pattern databases

Maintain segregated accounts separating platform funds from vendor settlement amounts

Document dispute resolution procedures meeting consumer protection regulations across operating jurisdictions

Pro Tip: Invest in compliance infrastructure during platform design rather than retrofitting systems after launch. Early implementation of automated verification workflows and fraud detection prevents costly remediation and regulatory delays that can halt marketplace growth.

“AI fraud detection has become essential infrastructure rather than optional enhancement, with 57% of payment providers now investing in machine learning capabilities to protect multi-vendor ecosystems from evolving fraud patterns.”

The Omnyfy Stripe launch partnership demonstrates how enterprise platforms integrate compliance-ready payment infrastructure, while evaluating marketplace options requires assessing built-in compliance capabilities. Understanding B2B ecommerce payment methods helps contextualise compliance requirements across different transaction types.

Managing refunds, disputes and multi-currency challenges efficiently

Post-transaction complexities test marketplace payment systems more severely than initial purchase flows. Refunds, disputes, and cross-border transactions create operational challenges that impact vendor satisfaction and platform profitability.

Partial refunds present the hardest automation challenge in multi-vendor carts where customers return items from multiple sellers. Your system must calculate proportional commission reversals, adjust payment processor fees, and determine which party absorbs transaction costs. Multi-vendor carts multiply these costs since each vendor’s portion requires separate processing, and fee structures rarely align with refund amounts.

Dispute and chargeback workflows require immediate commission reversal to prevent vendors receiving payment for contested transactions. When customers initiate chargebacks, your platform must freeze vendor payouts, gather evidence from sellers, and coordinate responses with payment processors. Failed dispute resolution results in permanent fund reversals that impact platform revenue and vendor relationships. Automated systems track dispute status, notify affected parties, and adjust financial records without manual intervention.

Delayed settlements create cash flow complications affecting both platform operations and vendor liquidity. When payment processors hold funds for risk assessment or rolling reserves, vendors wait longer for earnings while your platform must communicate timing expectations clearly. Enterprise marketplaces often establish reserve accounts covering potential refunds and disputes, tying up working capital that could fund growth initiatives.

Cross-border transactions introduce foreign exchange conversion, compliance with multiple regulatory frameworks, and varying settlement timeframes. PSD2, KYC, and AML requirements differ across jurisdictions, requiring localised verification workflows. Currency conversion fees erode margins, and exchange rate fluctuations between purchase and settlement create reconciliation challenges.

Best practices for refund and dispute workflows:

Implement automated partial refund calculations that proportionally allocate fees and commissions across vendors

Establish clear dispute escalation procedures with defined timeframes for vendor response and evidence submission

Maintain reserve accounts covering 5 to 10% of monthly transaction volume to buffer delayed settlements

Deploy real-time notification systems alerting vendors immediately when disputes arise

Create detailed audit trails documenting all refund and dispute actions for regulatory compliance and financial reconciliation

Common pitfalls and avoidance strategies:

Failing to automate commission reversals during refunds, creating manual reconciliation workload

Inadequate vendor communication about dispute processes, leading to poor evidence quality and lost cases

Underestimating cross-border compliance requirements, resulting in blocked transactions and vendor frustration

Neglecting to account for payment processor fee structures in refund calculations, eroding platform margins

Using single-currency systems for global marketplaces, forcing unfavourable exchange rates on international vendors

Multi-currency consideration | Compliance checkpoint | Operational impact |

|---|---|---|

FX conversion timing | Disclose rates before transaction completion | Vendor payout accuracy and customer transparency |

Cross-border KYC | Verify identity documents valid in vendor jurisdiction | Onboarding friction and regulatory compliance |

Settlement currency options | Allow vendors to choose payout currency | Vendor satisfaction and FX cost distribution |

Tax reporting | Generate jurisdiction-specific tax forms | Regulatory compliance and vendor tax obligations |

Payment method availability | Support local payment methods in each market | Conversion rates and customer accessibility |

The step-by-step ecommerce integration guide addresses technical implementation of refund workflows, while payment trends in ecommerce examines how B2B marketplaces handle complex refund scenarios. Understanding ecommerce and POS integration benefits helps contextualise omnichannel refund management.

Leveraging AI and pre-built payment platforms to enhance marketplace efficiency

Technology acceleration transforms multi-vendor payment operations from cost centres into competitive advantages. AI integration and pre-built platforms deliver measurable improvements in fraud prevention, operational efficiency, and time to market.

AI-powered fraud detection analyses thousands of data points per transaction, identifying suspicious patterns human reviewers miss. Machine learning models adapt to evolving fraud techniques, maintaining effectiveness as attackers change tactics. The 57% of payment providers now investing in AI capabilities recognise that automated fraud prevention reduces chargeback rates, protects vendor relationships, and preserves payment processor standing.

Pre-built payment platforms compress development timelines from 6 to 12 months of custom integration work to approximately 60 days using established APIs and compliance-ready infrastructure. These solutions eliminate the need to negotiate individual payment processor relationships, maintain PCI compliance infrastructure, and build commission calculation engines from scratch. The total cost of ownership decreases substantially when factoring in ongoing maintenance, security updates, and regulatory adaptation.

Interoperability between payment systems and existing enterprise infrastructure accelerates adoption and reduces implementation risk. Modern platforms offer pre-built connectors to major ERP systems, accounting software, and customer data platforms. This connectivity enables automated financial reconciliation, real-time reporting, and unified customer experiences across channels.

Ethical design principles emphasise inclusive payment options and transparent fee structures that don’t penalise underserved markets or vendor segments. Enterprise marketplaces implementing fair pricing models and diverse payment method support expand addressable markets while building vendor loyalty.

Key AI and automation benefits in marketplace payments:

Real-time fraud scoring reducing false positives that block legitimate transactions

Automated commission calculations handling complex tiered structures and promotional rules

Predictive analytics forecasting cash flow and identifying vendors at risk of churn

Dynamic routing optimising payment success rates by selecting processors based on transaction characteristics

Intelligent dispute management prioritising cases by win probability and financial impact

Automated compliance monitoring flagging regulatory changes requiring workflow updates

Pro Tip: Leverage AI-powered dashboards providing real-time visibility into payment health metrics, vendor performance patterns, and emerging fraud trends. Executive dashboards consolidating these insights enable data-driven decisions about payment strategy, vendor support priorities, and risk management investments.

The acceleration of commerce examines how AI transforms transaction speed and accuracy, while B2B ecommerce payment methods explores payment options driving conversion in complex sales cycles. When evaluating marketplace options, assess platform AI capabilities and integration ecosystems carefully.

How Ultra Commerce supports your multi-vendor payment strategy

Enterprise marketplaces require payment infrastructure that scales globally while maintaining compliance and operational efficiency. Ultra Commerce delivers a comprehensive platform purpose-built for complex multi-vendor operations.

Our multi-vendor marketplace platform integrates native payment routing, commission management, and settlement workflows that handle aggregated, split, and hybrid payment models without custom development. The composable architecture enables you to configure payment rules matching your business model, vendor tiers, and geographic requirements while maintaining a unified operational dashboard.

The enterprise ecommerce platform supports AI-powered fraud detection, automated compliance monitoring, and real-time financial reconciliation across global operations. Pre-built integrations with major payment processors, tax systems, and accounting platforms compress implementation timelines while ensuring regulatory compliance.

Explore how the Ultra Commerce platform transforms multi-vendor payment complexity into competitive advantage through intelligent automation and enterprise-grade security.

FAQ

What are the typical commission rates in multi-vendor marketplaces?

Commission rates typically range from 5% to 20% depending on product category, vendor tier, and marketplace positioning. Digital goods and services command higher rates while physical products with thin margins operate at lower percentages. Enterprise platforms often implement tiered structures rewarding high-volume vendors with reduced rates.

How long does it take to implement automated payment splits with platforms like Stripe Connect?

Pre-built platforms reduce implementation from 6 to 12 months of custom development to approximately 60 days. This timeline includes payment processor onboarding, API integration, commission rule configuration, and compliance verification. Complex requirements like multi-currency support or custom settlement schedules may extend timelines.

What compliance certifications are critical for multi-vendor payment platforms?

PCI-DSS Level 1 certification is mandatory for platforms processing over 6 million transactions annually. Additional requirements include PSD2 compliance for European markets, SOC 2 Type II for data security, and jurisdiction-specific licences for payment facilitation. Maintain current certifications to preserve payment processor relationships and market access.

How do marketplaces handle refunds involving multiple vendors?

Automated systems calculate proportional refunds based on each vendor’s cart contribution, reverse commissions accordingly, and allocate payment processor fees. The platform typically absorbs transaction costs unless vendor agreements specify otherwise. Partial refunds require sophisticated logic tracking which items were returned and adjusting settlements precisely.

Can AI reduce fraud and disputes in multi-vendor marketplaces effectively?

AI fraud detection reduces chargeback rates by 40% to 60% through real-time pattern analysis and risk scoring. Machine learning models identify suspicious behaviour across device fingerprints, purchase velocity, and historical patterns that manual review misses. The 57% of providers investing in AI capabilities demonstrate proven ROI through reduced fraud losses and improved payment processor relationships.